The worldwide semiconductor trade is liable to shortages and surpluses. Each drive capital investments. Throughout shortages, chipmakers broaden manufacturing capability, resulting in oversupply. Now, it’s a time of glut, and India is getting into the manufacturing fray with a $10-billion incentive package deal for the semiconductor trade. This raises the query of whether or not it ought to get into the ‘pink ocean’ of chip manufacturing, marked by intense competitors, or concentrate on chip design.

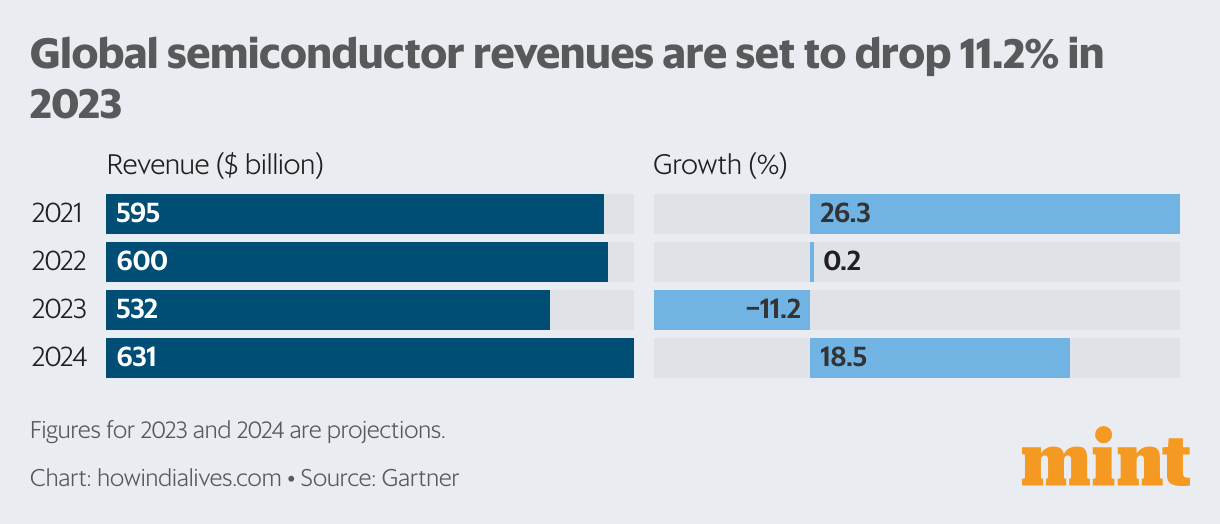

The oversupply is immense. Taiwan’s TSMC, the world’s largest chipmaker, reported a 23% drop in June-quarter (Q2) gross sales and warned that gross sales would drop 10% for 2023. Consultancy Gartner projected an 11.2% decline in revenues for the worldwide trade in 2023 after tepid 0.2% development in 2022. “As financial headwinds persist, weak end-market electronics demand is spreading from customers to companies, creating an unsure funding atmosphere,” it stated this April. The ache began when shortages through the pandemic was a glut final 12 months, worsened by fears of financial slowdown.

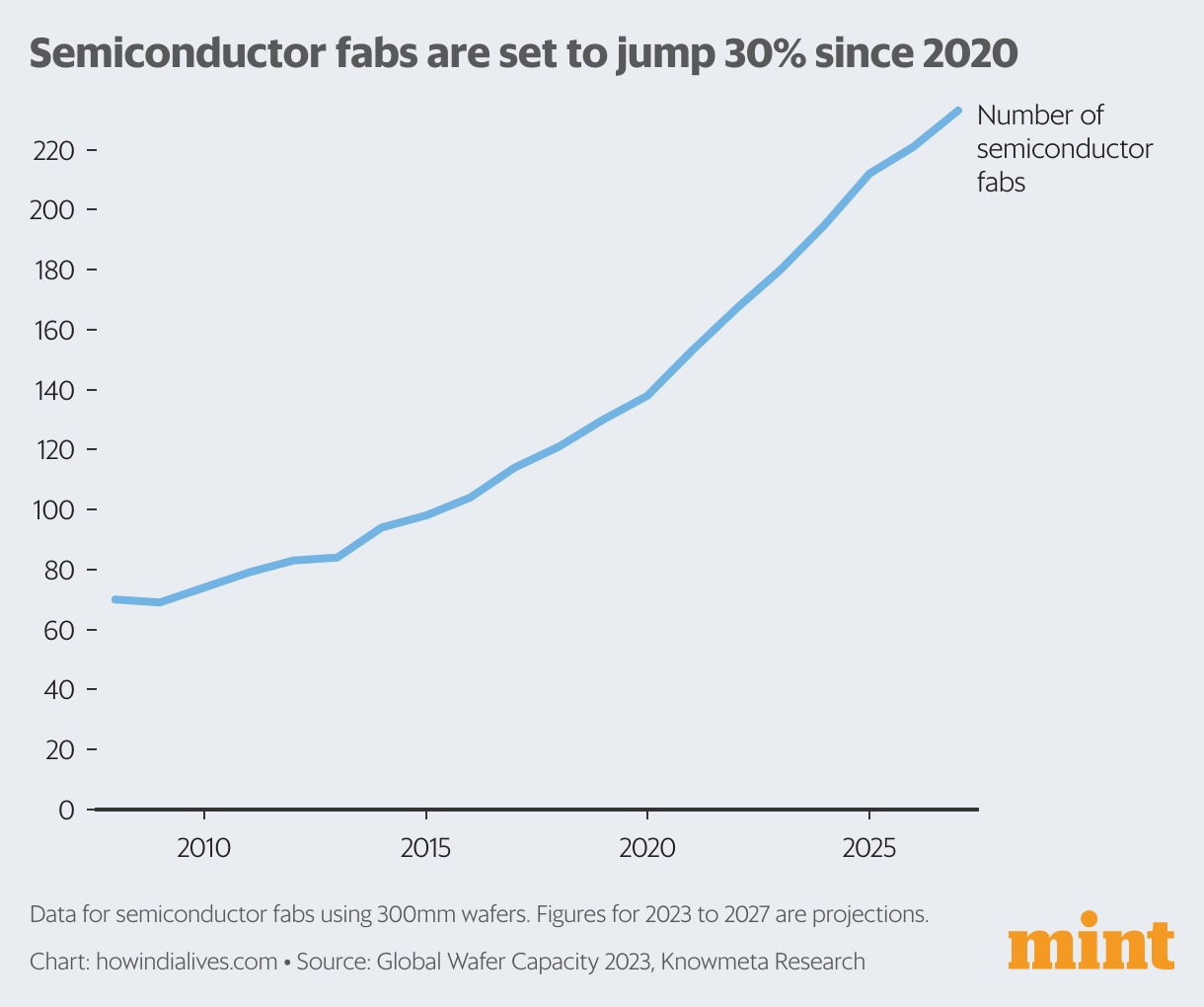

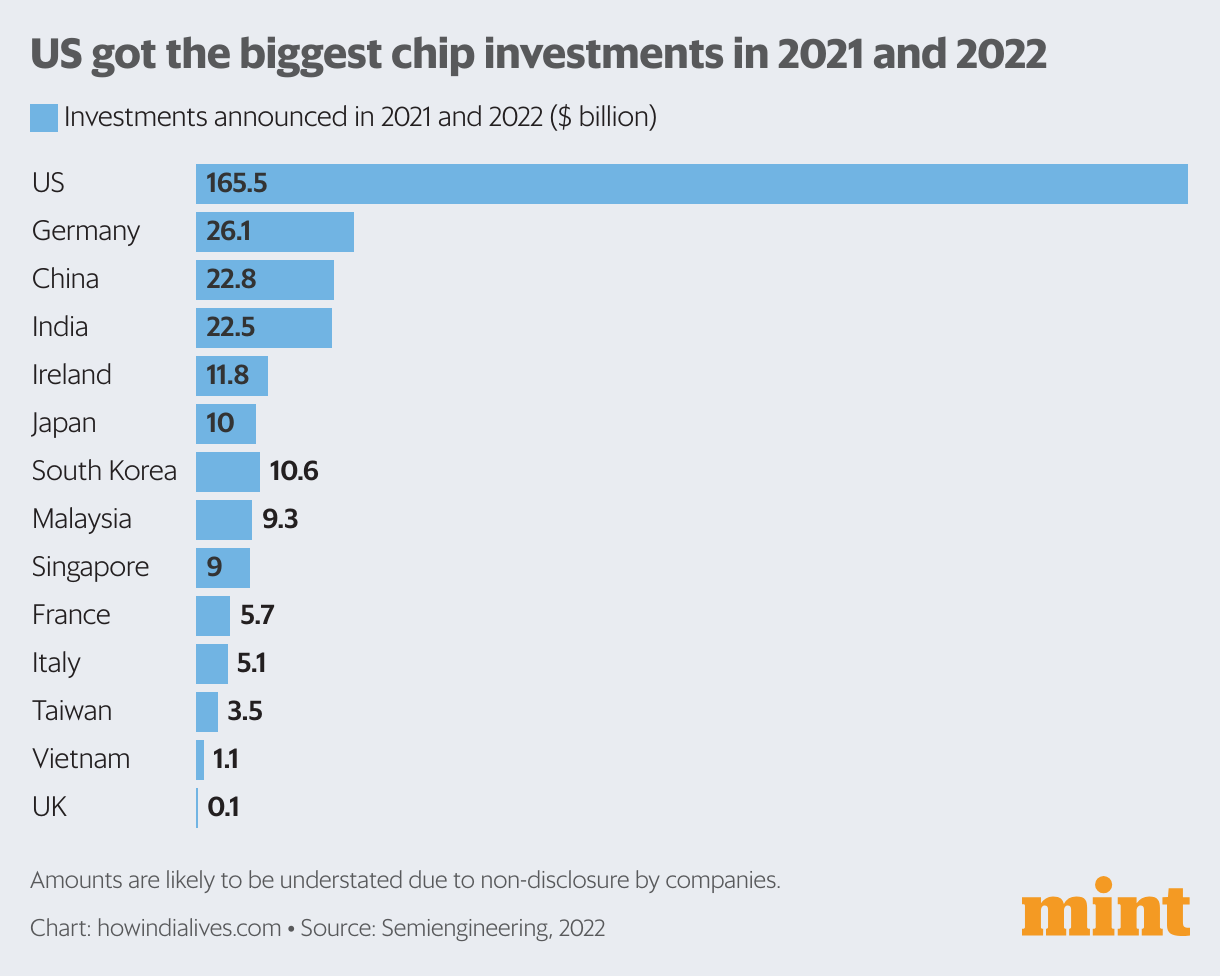

But, the sector is drawing huge investments. Earlier this month, the US stated firms there had introduced $166 billion in investments in semiconductors and electronics within the one 12 months since President Joe Biden signed off on a legislation that promotes the sector. In June, US-based Intel stated it will make investments $33 billion in Germany to broaden in Europe. The variety of semiconductor fabs processing 300-mm wafers globally is projected to leap from 138 in 2020 to 180 in 2023 and 233 in 2027. On this ocean, India too needs a spot.

Authorities push

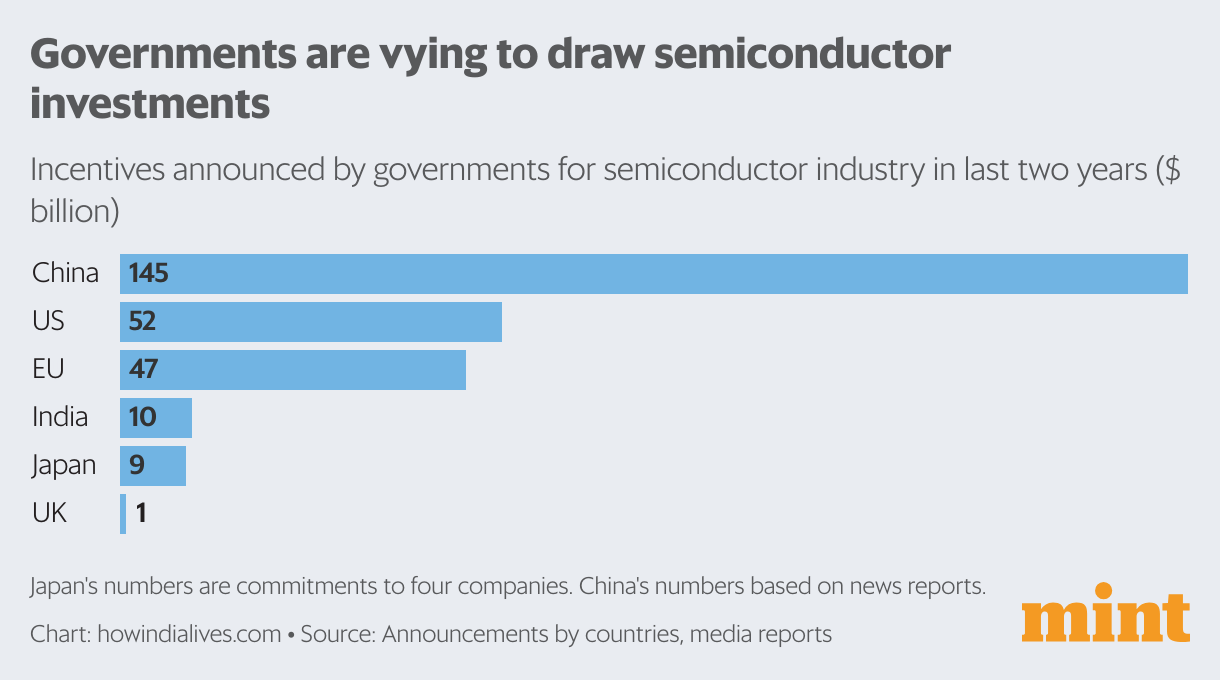

World competitors to construct chip manufacturing capability is pushed by governments. For instance, the US authorities’s CHIPS Act of 2022 supplies $52 billion in funding for semiconductor analysis and manufacturing. Final month, the European Union authorized its personal Chips Act, a 43-billion-euro ($47.5 billion) plan to develop extra fabs, aimed toward capturing “at the least” 20% of worldwide market share by 2030.

China is engaged on a $145-billion help package deal for its semiconductor trade, based on a Reuters report final December, and is facilitating simpler entry to subsidies, based on an FT report earlier this 12 months. Equally, South Korea, Japan and Taiwan supply tax credit, subsidize set-up prices and supply different incentives to advertise semiconductor manufacturing. It is pushed by each financial causes (like creation of jobs) and geopolitical causes (ongoing rivalry between the US and China). These twin forces are driving investments, regardless of the drop in revenues and extra stock.

Shifting stability

There’s been an imbalance within the international semiconductor trade because it entails enormous upfront investments. Many of those investments passed off in South East Asian nations and China. For instance, whereas the US accounts for 34% of worldwide demand for semiconductors, it accounts for under 14% of provide, based on McKinsey. Greater than half of US-owned fab capability is situated outdoors the US, based on Knowmeta Analysis. Japan, then again, accounts for 16% of provide and eight% of demand. Taiwan, the world’s high provider, accounts for only one% of demand.

The current push by numerous governments to fabricate regionally is anticipated to shift that stability, in addition to improve provide as soon as new capacities begin producing. Whereas it will guarantee a gradual provide of chips sooner or later, it has additionally raised considerations a few near-term expertise scarcity and value wars. If costs drop considerably, it might impair assumptions behind the returns on ongoing investments. Nevertheless, demand might outweigh these considerations.

Demand drivers

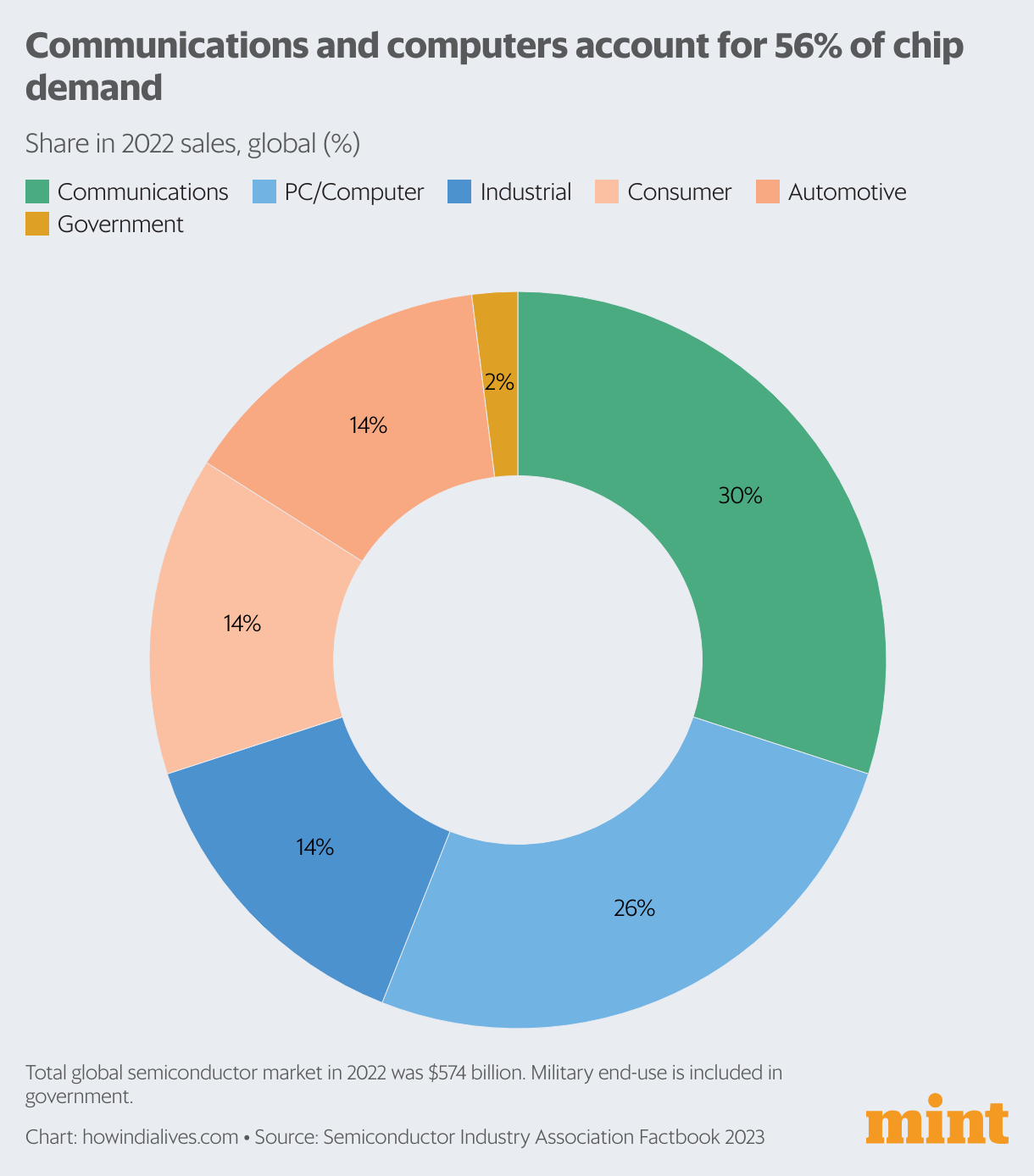

Communications and computer systems accounted for 56% of semiconductor gross sales in 2022 and automotive sector 14%, based on the Semiconductor Business Affiliation (SIA). McKinsey initiatives a tripling of demand from the automotive sector by 2030, fuelled by functions like autonomous driving and e-mobility. More and more, shopper demand for laptops and telephones is pushed by rising markets, together with these in Asia, Latin America, and Africa, SIA stated.

In keeping with a 2022 report by McKinsey, the worldwide semiconductor trade might see common annual development of 6-8% till 2030, reaching $1 trillion in measurement. Whereas semiconductor manufacturing is changing into a pink ocean, which is captured by the time period ‘chip wars’ that’s used to explain the rivalry between China and the West, the market itself guarantees to get greater. Thus, whereas the Indian authorities could also be betting on the suitable sector, the hot button is whether or not it may possibly flip the intentions and incentives into operational factories with out glitches.

www.howindialives.com is a database and search engine for public information.